It looks like we are in a recession. While a recession is not pleasant for anyone, I think that a recession is necessary to correct our trend of spending money we don't have.

It's no secret that the US personal savings rate has been falling for the past couple decades. It has even been negative.

Here is a chart showing the last half century of savings. You can see how in the mid-1980's it began it's 25 year negative trend.

There is a simple trade-off between savings and consumption: more savings and less consumption now, leads to more consumption in the future; less savings and more consumption now, lead to less consumption in the future. Basically, if we invest now (save), our investment will lead to faster growth and more wealth in the future.

Over the past two decades, Americans have chosen to save less and consume more. Interestingly, but not coincidentally, we have also enjoyed one of the longest periods of economic growth over the past two decades. We had a relatively small recession in the early 90's and another even smaller recession post 9/11. Other than that, our economy has been chugging along.

What has fueled this growth? I believe that some of the growth has come from the decrease in savings and increase in consumption. By saving less, Americans have increased consumption and at the same time fueled growth in GDP. Both the increased consumption and growth in GDP is SHORT TERM--it can't last forever.

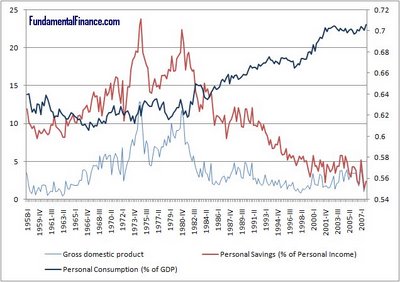

In the chart below, I compare historical data for three items:

1. The light blue line is year-over-year GDP growth.

2. The red line is personal savings as a percentage of personal income. Notice how it remains about the same distance from GDP growth until the mid-1980's, then personal savings decreases until it approaches zero. Before the 1980's, if GDP growth went up, the saving rate went up--people actually saved a higher percentage of their income when their income increased. After the 1980's people started saving less, regardless of GDP, and not only when GDP decreased.

3. The dark blue line is consumption as a percentage of GDP. Remember that GDP is made up of four components: consumption, investment, government spending, and net exports (exports minus imports). From 1950 through 1980, consumption as a percentage of total GDP was fairly steady. Then consumption began to take up a larger percentage of GDP -- in other words, growth in GDP was being driven by more consumption.

What was driving more consumption as a percentage of GDP? Decreased savings, of course! Over the past three decades, consumers have decreased the amount of money the spent--decreasing it a bit more each year. This fueled growth in consumption. So what happens when consumers no longer have any income dedicated to savings? They can no longer transfer savings to consumption. Then a valuable source of GDP growth dries up. Then we have a recession.

Hopefully the recession will serve a good purpose. The decrease in savings essentially represents a lifestyle change. Fundamental principles for giving mortgages have been abandoned--loans were even given at over 100% of a home's value. Home equity lines of credit have become common.

Credit card debt has sky-rocketed. These trends have enabled consumers to have more "stuff", even though they have no savings.

Right now, credit is tightening. It's getting harder to borrow money. This is a necessary adjustment to bring our consumption back to a reasonable level. Hopefully, people will get more nervous and begin saving more. Unfortunately, a recession is the only way we can make this adjustment. We have to consume less in the short run, which is going to adversely affect the GDP.

My question is, what is going to happen in the next two decades? I don't think that consumers are suddenly going to build the personal savings rate back up to previous levels. If we do, there will be a period of slower growth than the last two decades. If we hold our savings rate constant (at just above 0), then we're giving up future consumption and allowing foreigners to take all the gains.

It seems to me we're in a predicament.